We’re Not All In This Together

By Ray Kong

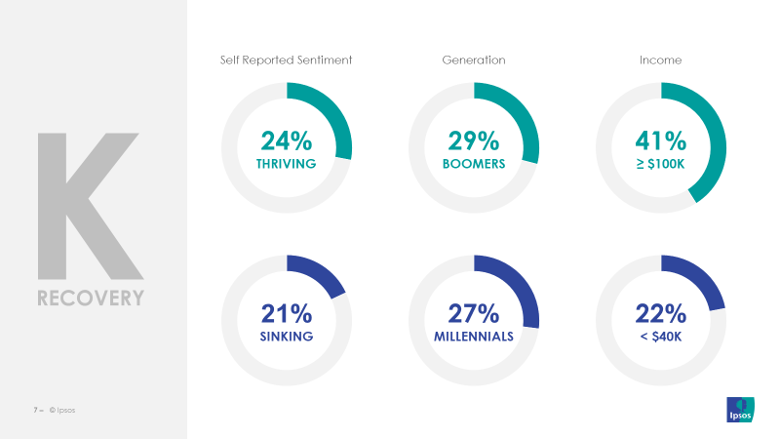

By now the phrase “K-shaped recovery” has entered the business lexicon as a way of describing the very clearly different circumstances experienced by different parts of the population throughout the pandemic. The pandemic has not treated all equally from an economic standpoint – some have thrived and some have struggled – and organizations need to recognize that these two disparate parts of the population need to be approached with distinct marketing and strategic approaches, as no one size fits all.

Part of the difficulty in actioning this lies in how to delineate membership in the upper and lower arms of the K. Three possible ways are:

– self reported sentiment (how do I feel about my current and future financial situation?)

– by generation

– by income

Properly, one would create statistically robust segments using a combination of these three dimensions and include gender and other socio-demographic variables; but in the absence of that, income and generation are easy to use as proxies.

Upslope strategy should be to grow and retain these customers. Demographically, these Canadians are more likely to be homeowners, and are older. They have been fortunate to see large growth in absolute dollar terms in savings and net worth over the last 15 months and therefore they are satisfied with their current and future financial situation. Having thrived and saved through the pandemic, we expect that they will exit as ‘spenders’ and how quickly they return to spending including on luxury items, big ticket items and vacations, will be instrumental to how and how fast the economy rebounds.

We suggest that activity with respect to this group should include:

- Understanding motivations to help unlock savings and other investments to stimulate spending. For example, am I saving for a big ticket item or will I spend more on smaller items? Am I saving for longer-term luxuries or for shorter-term every day expenses?

- Placing ESG program and message emphasis on the environment and social improvement. Those on the upslope have personally done well through the pandemic but perceive that environmental issues have taken a back seat and fractures in society have formed.

- Understanding urban out-migration patterns at a granular level to derive implications on retail locations and service availability. For example, where are the geographies of growth? And who are moving there with what needs and potential?

Downslope customer strategy should be focussed on managing the cost to serve. We suggest that this group should be the input group for creating, adopting, and testing digital innovations as demographically this generally is a younger group and to the extent that we know them, they skew female and visible minority. They have seen growth in their savings over the last 15 months, however the average amounts are low in absolute dollar terms. Satisfaction with their current personal financial situation is low and we expect that this group will exit the pandemic as ‘savers’. What discretionary spending they do, will be driven by value (not just cost but also including convenience and quality).

We suggest that activity with respect to this group should include:

- Advising on debt management, simple savings methods, and general financial literacy. Some are coping with under-employment as stimulus programs end. Others have taken on new debt to finance their out-migration and still others are re-evaluating lifestyle and working to understand the financial implications.

- Better understanding use and growth of digital shopping ecosystems including embedded POS financing. We suggest that using this early adopter to gauge what digital innovations are being embraced versus those which are shiny new toys, while driving down cost-to-serve is a win-win.

- Placing ESG message and program emphasis on social and income equality issues. Downslope consumers continue to place importance on environmental issues, but because they have not thrived through the pandemic, and they feel at the short end of the income equality stick, efforts in this direction are meaningful to them.

These are only high level examples to illustrate that we are most definitely not ‘all in this together’ and that the organizations need to be evidence-based and strategically deliberate in their tactics for each of the two arms of the K for future success.

About the Author:

Ray Kong is an experienced marketer with over 25 years of experience in both consulting and at the executive level of major Canadian corporate institutions. As a senior client partner with Ipsos, he currently serves clients in a number of different sectors in customer experience, brand development and measurement, operational improvement and strategy work and acting as a hub to bring the best of Ipsos’ work around the world to local clients. Ray is a published academic author and served three years as an adjunct professor of marketing at York University in Toronto and speaks regularly on consumer trends, marketing trends and best practices of organizations in customer experience, ethnic marketing and loyalty. He has a BSc from the University of Toronto and an MBA from York University in Toronto.